Two of the sharpest minds in the trading community sat down to dissect what is arguably the most complex market environment of the past decade. In the latest episode of Charts and Shacks, Alvaro Pereira and Donny break down the structural shifts driving the semiconductor sector, where AMD really stands against Nvidia, and whether the beaten-down names — Micron, SanDisk, and Netflix — are genuine dip opportunities or value traps. Here is what every trader needs to understand right now.

The DRAM Mania: Cyclicality Always Knocks

The episode opens with a stark warning about DRAM names. Stocks in this sector have gone parabolic over the past few months, fueled by an insatiable demand for memory to power AI data centers. But Alvaro and Donny are quick to remind investors that these are inherently cyclical businesses — and cyclicality does not care about momentum.

“Cyclicality will eventually kick in,” Donny warns. While these stocks can defy gravity longer than most expect, the eventual reversal tends to be severe. There is currently a greater-than-50% probability that some of these names could be cut in half by year-end. This is not a call to short — shorting a bubble is a dangerous game — but it is a strong call for discipline.

Managing Position Size in an Overextended Market

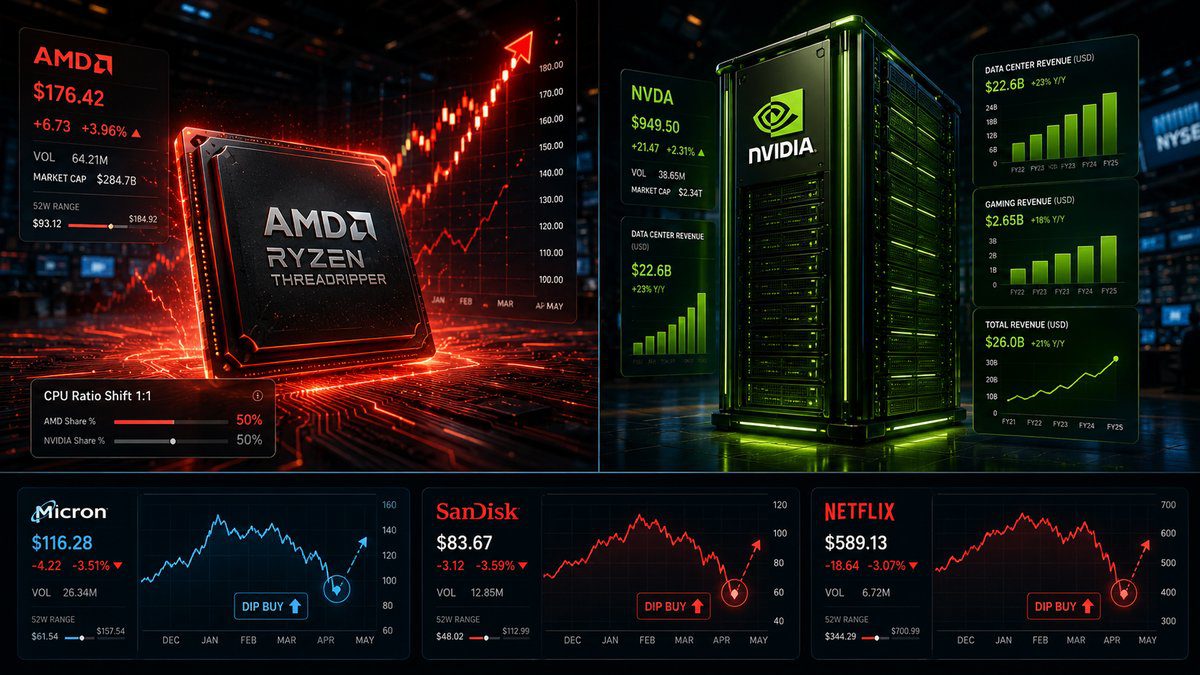

The technical overextension in names like SanDisk is almost unprecedented. At the time of recording, SanDisk was trading 24% above its 20-day moving average. To put that in perspective: the stock could enter a technical bear market — a 20% drawdown — and still be in a macro uptrend.

Because of this elevated volatility, the hosts recommend a strict Utility-First approach to position sizing. If your standard position size is 2% of portfolio, consider cutting it in half. In a market where individual stocks move 8% in a single session, survival depends on not being overexposed when the reversal arrives.

AMD vs. Nvidia: Is Lisa Sue Stealing the Crown?

The most debated question in the trading community right now: can AMD actually compete with Nvidia for AI dominance? A year ago, the consensus was that Nvidia held a five-year lead. Has that gap narrowed?

The Leftover Theory

Donny’s take is nuanced. AMD is not necessarily stealing customers from Nvidia in the traditional sense — Nvidia is simply so booked out that customers are turning to AMD for what’s available. “We’re going from one cut of meat to another nice cut of meat,” he explains. The addressable market is large enough that both can win.

The numbers back this up. AMD grew revenue 38% year-over-year — a strong print by any standard. But Nvidia is running at 70–75% growth with elite net income margins. The market cap differential exists for a reason.

The 1:1 Ratio — The Real Catalyst

The real driver behind AMD’s recent 15–20% gap-up was not a GPU breakthrough. It was a fundamental shift in data center architecture. Historically, the CPU-to-GPU ratio in AI infrastructure was 1:4 or even 1:8. Lisa Sue highlighted that the industry is moving toward a 1:1 ratio as agentic AI workloads place greater demands on the entire compute stack.

This matters enormously. Nvidia dominates the GPU side. But a 1:1 ratio means a dramatic increase in demand for high-performance CPUs — which benefits AMD and Intel far more. The market is only beginning to price this in.

Technical Deep Dive: Buying the Dip or Chasing the Top?

AMD recently showed a classic bearish RSI divergence: price made a higher high while momentum made a lower high. The “gust” is fading. The level to watch is a clean retest of the 50-day moving average or the $376–$378 zone before considering a long entry.

Nvidia reports earnings on May 20th and the chart looks constructive heading into the print. The risk, however, is a “sell the rip” pattern regardless of the beat — at near $5 trillion market cap, the hurdle for a significant post-earnings move is enormous.

Qualcomm is no longer just the iPhone chip company. The company is pivoting hard into agentic AI at the edge — smart glasses, on-device inference, next-generation handsets. Revenue growth has been muted, but the market is beginning to price in a transformation similar to what drove SanDisk’s re-rating. At 19x forward earnings in a sector of extreme multiples, Qualcomm remains compelling.

Netflix: The AI Disruption Narrative Does Not Hold Up

Perhaps the most provocative segment of the episode takes on the bear case for Netflix. The stock has sold off partly on the narrative that generative AI will democratize movie production — allowing anyone to create high-quality content and erode Netflix’s competitive edge.

Alvaro and Donny dismiss this thesis directly. The idea that amateur AI-generated content will compete with Netflix’s distribution infrastructure, production budgets, and global subscriber base is not a serious argument. Netflix is the only streaming company consistently generating profit. The more likely outcome: Netflix uses AI to reduce its own production costs and widens its moat rather than being replaced by it.

Technically, Netflix is broken below its 100-day EMA. The level to watch for a potential re-entry signal is a recapture of the $95–$100 zone, which would confirm the breakdown as a false move rather than the start of a sustained decline.

Key Takeaways for Traders

- DRAM and memory names are technically overextended — reduce position size, not conviction, if you hold them

- AMD’s catalyst is the CPU-to-GPU ratio shift toward 1:1, not GPU market share theft from Nvidia

- Nvidia’s chart is strong into May 20th earnings, but expect volatility regardless of the result

- Qualcomm at 19x forward earnings is the lowest-multiple play in the AI hardware ecosystem

- Netflix’s AI disruption bear case is overblown — watch the $95–$100 recapture for a re-entry signal

- If you are sitting on 100–200% gains in semiconductor names, trimming is not weakness. It is professional trade management.

The market is pricing in years of future growth today. The traders who survive this cycle will be the ones who had an exit strategy before they needed one. Master the setup. Manage the risk. That is the edge.

Video Credit

Analysis originally presented by Bilingual Stock Market Channel and Gorilla with Glasses. Watch the full session below.